In Southeast Asia’s semiconductor race, Vietnam and Malaysia are emerging as strategic rivals.

Malaysia boasts decades of leadership in assembly, testing and packaging. Its 10-year national semiconductor strategy, launched in 2024, is ambitious. But it lacks detailed milestones beyond 2035, reflecting a more short-term to medium-term orientation.

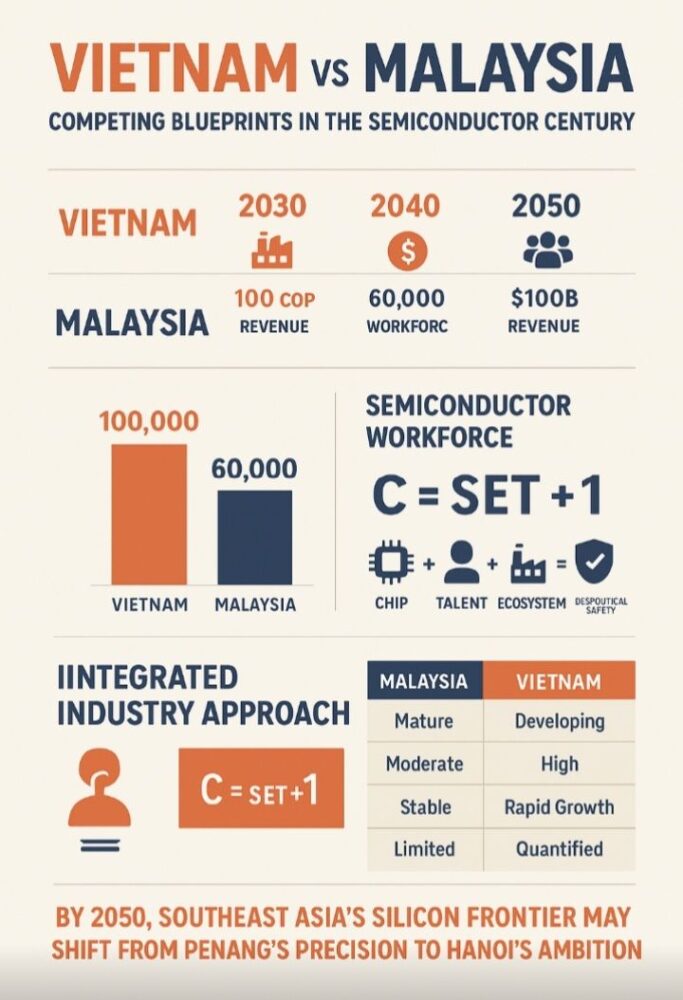

By contrast, Vietnam’s long-term semiconductor roadmap presents a more structured and ambitious national vision extending to 2050. Its three-phase plan lays out concrete numerical targets for company growth, facilities, workforce development and revenue (LuatVietnam, 2024).

Vietnam’s 2050 vision vs Malaysia’s 2035 roadmap

Vietnam’s semiconductor development framework features distinct phases – to 2030, 2040 and 2050 – each with quantifiable benchmarks for industry size, number of firms, trained specialists and total output. The country targets industry revenue exceeding $100bn by 2050, setting intermediate milestones every decade (Modern Diplomacy, 2024).

Meanwhile, Malaysia’s national semiconductor strategy articulates aspirations for global leadership in packaging and design services. But it does not specify comparable long-term revenue goals.

- Sign up for Aliran's free daily email updates or weekly newsletters or both

- Make a one-off donation to Persatuan Aliran Kesedaran Negara (ALIRAN), Maybank a/c 507246118995 or CIMB a/c 8004240948

- Make a pledge or schedule an auto donation to Aliran every month or every quarter

- Become an Aliran member

This difference in time scope is not merely symbolic. It reflects different strategic cultures.

Vietnam’s structured roadmap suggests a developmental-state model emphasising industrial planning and measurable outcomes.

Malaysia’s strategy reflects a liberal-institutional framework that relies on private-sector dynamism and foreign partnerships without rigid quantitative targets.

A recent public-private partnership is exemplified in the Selangor government’s initiative through the Selangor Information Technology and Digital Economy Corporation and Permodalan Negeri Selangor Bhd, partnering Artem Venture Fund. They have established a Selangor semiconductor fund, known as Ehsan Capital, to empower the industry.

The close collaboration between compradore enterprises and state capital with multinationals – a diversion from the national strategy’s core objectives – is reflected in the deluge of infrastructural platforms in the country. Malaysia has attracted RM185bn ($44bn) in investments in data centre-related projects between 2021 and 2024 (Iseas-Yusof Ishak Institute).

However, the sustainability concerns – in electricity and water supply adequacy essentials – could jeopardise these hubs of server databases’ momentum. They could also result in the country losing focus on the ongoing fierce battle for semiconductor competitiveness.

Workforce depth and productivity

Human resources remain a critical factor in determining national competitiveness in semiconductors.

Here, Vietnam’s talent blueprint appears more detailed and future-proof. Its plan calls for 50,000 semiconductor engineers by 2030 and over 100,000 by 2040. It has detailed segmentation by education level, specialisation and training institutions (Vietnam Law Magazine, 2024).

This systematic approach signals a long-term investment in total factor productivity – a measure of economic efficiency that captures how well a country converts inputs like labour and capital into output. Vietnam’s approach embeds skill accumulation and knowledge processes into industrial planning.

Malaysia, by contrast, aims to produce 60,000 engineers under its semiconductor strategy. But the target lacks disaggregation by specialty or training pipeline.

Malaysia’s education–industry coordination remains fragmented, with limited research and development integration across universities and semiconductor firms (The Interpreter, 2025). This weakens Malaysia’s productivity chain, as process knowledge and design expertise remain externally sourced.

Without stronger university–industry linkages and incentives for postgraduate research, Malaysia risks remaining in the middle-value segment of the global chain.

Technological integration: Vietnam’s formula

Vietnam’s semiconductor strategy introduces a compelling conceptual formula – “C = SET + 1” – which integrates specialised circuits (S), electronics (E), and talent (T) into a cohesive ecosystem. The “+1” represents Vietnam’s added value as a safe and reliable supply chain destination (TheLeader, 2024).

This formula encapsulates a holistic approach linking design, manufacturing and logistics to geopolitical positioning.

By contrast, Malaysia’s integrated circuit design and front-end manufacturing initiatives are still in pilot stages, fragmented between regional industrial clusters in Penang, Kulim and Johor.

While Malaysia’s assembly, testing and packaging infrastructure remains world class, its value chain integration remains vertically limited – strong in packaging and testing but weak in upstream design, materials and fabrication.

A Brazilian–Malaysian partnership began in 2023 following a semiconductor event in Kuala Lumpur. But despite Prime Minister Anwar Ibrahim’s follow-up meeting with Brazilian President Luiz Inacio Lula da Silva in November 2024 and participation in the G20 summit under the presidency of Brazil that year, the partnership has not yet shown concrete progress (STORM, 2024).

Geopolitical catalysts and strategic partnerships

Vietnam’s trajectory is boosted by geopolitics.

The Vietnam–US Comprehensive Strategic Partnership, announced in September 2023, triggered a surge of foreign investment in Vietnam’s semiconductor sector (Vietnam Briefing, 2024).

American giants, including Synopsys and Marvell, have expanded design centres in Ho Chi Minh City, aligning Vietnam’s industrial rise with the US ‘friendshoring’ doctrine to diversify semiconductor supply chains away from China.

Malaysia’s national semiconductor strategy also benefits from strong partnerships with Arm Holdings, Intel, Infineon and GlobalFoundries.

Yet its geopolitical positioning remains less pronounced. It seeks neutrality between the US and China, balancing between Washington’s Chips Act supply chain diversification and Beijing’s Belt and Road technology ecosystems.

While this neutrality offers flexibility, it also reduces Malaysia’s bargaining power in securing preferential strategic investments tied to Western reshoring policies.

Challenges and structural constraints

Both countries face systemic challenges.

Vietnam currently employs only around 6,000 semiconductor engineers and faces infrastructure deficits, particularly in power supply and logistics (Modern Diplomacy, 2024).

Malaysia, meanwhile, confronts talent shortages, limited R&D commercialisation and bureaucratic inertia. Despite decades of experience, its innovation output remains constrained by low domestic reinvestment of semiconductor profits, with much of the value captured by multinational companies.

From a structural-political economy perspective, Malaysia’s semiconductor success has historically depended on compradore arrangements – foreign capital partnerships mediated through state-linked firms.

Vietnam’s emerging model, by contrast, reflects a developmental capitalism framework with central coordination and performance-based incentives. This may give Vietnam greater policy coherence in scaling up the value chain by 2045.

Divergent yet interlinked futures

By mid-century, the regional semiconductor landscape may look markedly different.

Malaysia will likely remain a trusted hub for high-precision packaging and automation systems, while Vietnam could evolve into a full-spectrum semiconductor ecosystem – from design to advanced manufacturing.

Vietnam’s explicit national goals of completing the semiconductor value chain by 2045 and establishing itself as a global talent hub by 2030 signal an intent to compete directly with Malaysia in higher-value segments once its initial growth phase stabilises after 2025.

The difference between the two – Malaysia’s reliability and infrastructure versus Vietnam’s scalability and cost optimisation – defines ASEAN’s semiconductor competitiveness.

Yet in strategic terms, Vietnam’s clarity of vision, measurable outcomes and geopolitical alignment with US supply-chain diversification may grant it a decisive edge in shaping the region’s semiconductor future.

AGENDA RAKYAT - Lima perkara utama

- Tegakkan maruah serta kualiti kehidupan rakyat

- Galakkan pembangunan saksama, lestari serta tangani krisis alam sekitar

- Raikan kerencaman dan keterangkuman

- Selamatkan demokrasi dan angkatkan keluhuran undang-undang

- Lawan rasuah dan kronisme